I am very happy to share this article on downtown multifunctionality/ functional diversity that was recently published in the JURR, a British journal focused on urban renewal and regeneration. It reflects my most recent thinking on this subject, as well as my efforts to add some analytical heft to it while also getting more people to find it of interest and importance.

Here’s the abstract: “In the large downtowns in the US, the adaption rates and impacts of remote work have been strong and sparked efforts to make these districts far more multifunctional, especially by adding lots of new housing. While comparable city centres in Western Europe have not seen remote work have similar impacts on office occupancy, multifunctionalism has long been heralded as a factor that makes them strong. For example, it underpins their two key competitive advantages of dense agglomeration and the generation of many multipurpose trips. While multifunctionalism is a familiar concept and is often mentioned in relevant publications, there is amazingly little written about it theoretically, and little to no empirical research done on it. I took on that topic in a recent paper in which I noted that how downtown multifunctionality is ‘packaged’ in the physical containers in which the venues of these functions are activated, and how they physically relate to each other, are very often the key factors in determining whether efforts to make a downtown more multifunctional will succeed. I also argued that a function must have very magnetic destinations active in these containers. This paper focuses just on the topic of packaging functions and is an expansion of my prior analysis that covers much new ground.”

I am proud to share with you my article “How Our Downtowns’ Three Most Important User Groups Can Help Their Sustained Recoveries” that was recently published in the IEDC’s Economic Development Journal. It focuses on downtown workers, residents and visitors and covers our largest downtowns as well as those of more modest size. It presents several analytical conclusions that counter conventional wisdom. For instance, while the media have focused on the reduced presence of downtown workers in our largest downtowns, the drop in downtown visitors was far larger, and smaller downtowns were less impacted by remote work because they are not usually the primary locations for their cities’ office prone workers.

The article relies heavily on data from the CCD’s Downtowns Rebound project led by Paul Levy, Placer.ai, OnTheMap, and my field experiences, as well as a dataset created by Bill Ryan on all the cities with population between 25,000- 75,000 in seven Midwest states.

Non Resident Downtown Employees. Three plus years after Covid19 was declared a national emergency, it seems that most of our downtowns are now pretty far into recovering from its impacts, though their recoveries are not yet complete. Even so, fears of a Doom Loop emerged grounded mainly on the negative impacts of remote work on office demand, that in turn is based on some distortedly presented data from Kastle Systems on office building worker occupancy rates. Kastle reports on metro regions, not cities though they speak of cities, and the vast majority of their buildings are in the suburbs, not downtowns. Also, when they do have some presence in a downtown, they tend to be in the second tier buildings most likely to have been made outmoded by remote work, not the most attractive and successful ones. In Manhattan for example, Kastle is not in the higher quality buildings owned by the city’s 10 largest landlords that attract the most prestigious tenants and have the highest rents.[1] Flaming the Doom Loop fears was an academic study that showed how such a reduction in office occupancy in NYC and nationally would severely reduce property values by about 44%, with commensurate resulting reductions in municipal property tax revenues.[2] To date, such drastic reductions have not appeared to gain much traction in NYC or nationally.

The most reliable data on remote work is from WFH Research. It shows that about 41% of the workers it sampled work totally remote (12%) or in a hybrid mode (29%). Moreover, about 33% of the paid full days were worked from home in our largest cities. So yes, remote work has reduced the number of hours office workers are in our downtowns, but most are still working there. And the 33% is far less than the 60%+ hours worked at home early in the crisis. So office workers have slowly been contributing to the recoveries of their downtowns by working more often in their downtown offices, if not at precrisis levels.[3]

That said, the data strongly support the hypothesis that a significant amount of remote work is here to stay, and corporate execs and downtown leaders committed to achieving a 100% Return To Office (RTO) rate may be digging a ditch for themselves by fiercely fighting remote work. What they also probably overlook is that precrisis the office buildings in these large downtowns never had a 100% worker occupancy rate. An 100% rate would mean that workers were not sick, on vacation, doing their jobs by meeting externally with clients and suppliers, or working from home.

Consequently, it is really hard to understand those who continue to want a 100% RTO rate and the extinction of remote work, since evidence strongly indicates that quest is impossible to achieve, and it probably never even existed before Covid19. Certainly, one can question whether a recovery strategy primarily aimed at achieving precrisis office occupancy rates would be productive.

Furthermore, we don’t know clearly yet how that 33% reduction in paid days worked will translate into office demand. One might reasonably suspect that it makes a lot more buildings outmoded. Yet, there is a real possibility that the effects of remote work might be mitigated to a significant degree by higher SF/worker in offices reconfigured to be more attractive to workers and heighten a firm’s RTO rate. A current primary strategic challenge for our large downtowns is how to make up for the spending and pedestrian trips of the 41% of office workers who are now working at home to a significant degree. That is what downtown leaders should now be focusing. on, not raising RTO rates.

Downtown Housing. More housing is certainly one way of doing that, but it will take a lot of time, gobs of money, new regulations, and a lot of tough politicking to achieve. It will certainly not be easy.[4] That said, it definitely still should be done, but we now need another strategic thrust capable of producing meaningful shorter term benefits.

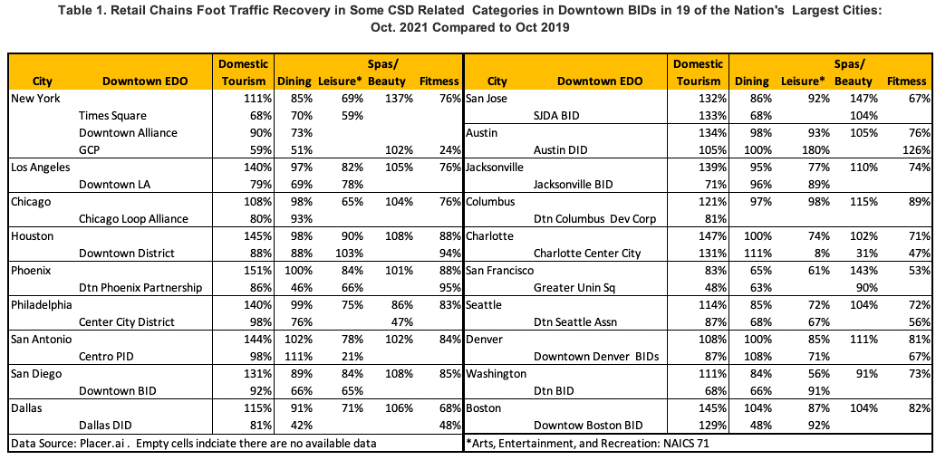

Downtown Visitors. To achieve more immediate results, another, and more practical, strategic thrust should be to increase downtown visitation by those who neither live nor work there. Data released by Philadelphia’s Center City District –see Figure 1 above –show that such visitors account for most downtown visitation and by a large margin.[5] Based on the data in Table 1 that shows domestic tourism was returning very strongly at the municipal level in 19 of our largest cities and in several of their downtowns—e.g., Austin, Boston, Charlotte, San Jose, and Philadelphia – as early as October 2021, my very strong suspicion is that researchers will soon report that this pattern characterizes many other large downtowns.

Foreign and business tourism are also recovering, but at lower rates that may take some time to regain precrisis levels, if they ever do. Business travel budgets, for example, are rebounding, though reflecting in part higher travel prices. Moreover, about 17% “of corporate travel will be replaced with virtual meetings, …suggesting a degree of permanence in the shift with companies recognizing the benefits of virtual meetings ranging from cost savings to lower carbon footprints.”[6] Still, foreign and business tourists had almost completely disappeared from our large downtowns early in the crisis, so their returns, even if at a level lower than might be desired, have been meaningfully contributing to downtown recoveries.

Strong Destinations Are Needed to Win More Visitors. My research and field visits over the past few years has led me to believe that many of our largest downtowns need to up their game when it comes to downtown visiors:

They have been living off of their laurels and too many of the attractions downtown leaders have seen as strong and unique have in fact lost their luster and a significant amount of their magnetism.

These old attractions/destinations now need a hard-headed assessment, and then where required they should be improved or replaced. People come downtown based on the strength and convenience of its attractions.

Improving the programming of public spaces may be one element of such a thrust. Improving the tenants of the small shops on side streets might be another. Right now many rely primarily on retail windows to make sidewalks interesting. Can other uses capable of doing that be brought in?

In many of these large downtowns these attractions’ ability to bring in visits by people living and working within between .25 mi and 1 mile of the core has significantly atrophied over the past 10 years or so. THESE RESIDENTS ARE NOW BEING UNDERSERVED, YET ARE WITHIN REASONABLE WALKING AND BIKING DISTANCES. They should be given priority attention.

[5] In Placer’s calculations: “Visitor” = shopper, tourist, convention attendee, concert attendees, someone visiting a doctor, etc. Resident = Their phone sleeps in the geography most nights per week. Non-Resident Worker = Their phone sleeps in a different geography at night, but routinely comes to the same location in the defined area 3-5 days per week. I want to thank Paul Levy for generously sharing these data with me.

Rob Steuteville, the editor of CNU’s journal Public Square, recently interviewed David Milder about his article in The ADRR, Strong Central Social Districts: The Keys to Vibrant Downtowns. The interview was published on the Public Square website in two parts, on August 17th and 23rd. David thanks Rob for his great questions that helped him explain more fully CSDs and their importance.

Save the date for: Bringing Back Downtown Retail After COVID-19

Across the nation in downtowns large and small, leaders and stakeholders are beginning to ask questions such as:

Where will retail be in downtowns like ours as we recover from this very stressful crisis?

What are the best opportunities for regaining, and possibly increasing, the strength of our downtown’s retailing?

What strategies, projects, and programs can help us achieve those potentials?

To address these critical questions, the American Downtown Revitalization Review- The ADRR – is partnering with the University of Wisconsin Madison – Extension to present an online panel discussion on Bringing Back Downtown Retail After Covid19 on:

Wednesday.

October 6, 2021,

at 12:30 pm CST.

The focus will be on downtowns and Main Street districts in communities under 75,000 in population. The webinar is part of Extension’s Learning from the Experts series. The panel will include three nationally known experts: Michael J. Berne of MJB Consulting, Kristen Fish-Peterson of Redevelopment Resources, and N. David Milder of DANTH, Inc. Bill Ryan of UW Madison-Extension will moderate the session. Stay tuned for details about signing up for the Zoom link needed to attend.

No, We Are Not Facing a Restaurant or Retail Industry Apocalypse

By N. David Milder

An Introductory Overview.

While the economic impacts of Covid19 are culling the weaker firms in the industries that frequently occupy downtown storefronts, and permanent closure rates are probably higher than those during the Great Recession, they are not anywhere near reaching the apocalyptic levels that would involve the effective decimation of these industries and impair their recoveries. Claims of industry apocalypses seem to be the rage in recent years starting with retail before the crisis. Since Covid19’s appearance the restaurant, personal services, and arts industries have also been seen in that light – often by industry leaders who are desperate to gain public attention and win strong government financial support for their member firms.

Many of the reported closures did not reflect economic failure, but legal necessity, and these operations reopen quickly when allowed by local regulations. A more accurate view of the situation should be based on the fact, as established by a research team from the Federal Reserve, that business deaths are a normal occurrence with about 7.5 percent of firms and 8.5 percent of establishments exiting annually in recent years.[1] They also noted that small firms account for most of these closures. The team also found that “temporary business closure is common, affecting about 2 percent of establishments per quarter.” Covid19, as many crises do, has accelerated the processes of creative destruction that were already taking root in these industries prior to this crisis. Even if the permanent closure rates prove to be relatively higher than those produced by the Great Recession, there is no evidence that they will be so strong that they will prevent vibrant recoveries.

[1] Crane, Leland D., Ryan A. Decker, Aaron Flaaen, Adrian Hamins-Puertolas, and Christopher Kurz (2021). “Business Exit During the COVID-19 Pandemic: NonTraditional Measures in Historical Context,” Finance and Economics Discussion Series 2020-089r1. Washington: Board of Governors of the Federal Reserve System, https://doi.org/10.17016/FEDS.2020.089r1.

As the readers of this blog probably know, I have spent a lot of time and effort on identifying the components of our Central Social Districts and analyzing what makes them succeed or fail. I’ve dug deeply into public spaces, movie theaters, housing, and various other components in cities large and small.

Recently, I was asked for one article that put it all together. I realized that I did not have one, so I consequently set out to write it. That article was recently published in The American Downtown Revitalization Review – The ADRR at https://theadrr.com/

Doing the topic justice meant that it would be long, about 30 pages, and more like a monograph than an article. Readers wanting a quicker take can just focus on the first six pages. However, if you are looking for more guidance about what to do and not do, you will need to dig deeper into the article.

Some of the important things I tried to do are to establish that some components are much easier and cheaper to establish than others, and which work better in different types of downtowns. I also tried to strip away a lot of the advocacy hype about some components that too often hides the challenges involved and obscures how progress needs to be evaluated, e.g., the arts venues, while spotlighting venues whose importance still goes widely unrecognized, e.g., libraries.

Here’s the article’s tease and link:

Strong Central Social Districts: The Keys to Vibrant Downtowns

By N. David Milder

DANTH, Inc.

CSDs and Some of Their Frequent Components. Since antiquity, successful communities have had vibrant central meeting places that bring residents together and facilitate their interactions, such as the Greek agoras and the Roman forums. Our downtowns long have had venues that performed these central meeting place functions, e.g., restaurants, bars, churches, parks and public spaces, museums, theaters, arenas, stadiums, multi-unit housing, etc. The public’s reaction to the social distancing sparked by the Covid19 pandemic, and the closure of so many CSD venues, was a natural experiment that demonstrated how much the public needs and wants these venues. They are the types of venues and functions that make our downtowns vibrant, popular and successful. To read more click here : https://theadrr.com/wp-content/uploads/2021/07/Strong-Central-Socia-LDistricts-__-the-Keys-to-Vibrant-Downtowns__-Part-1-FINAL.pdf